Kenya’s digital payments journey, spearheaded by M-PESA and guided by the Central Bank of Kenya, has driven significant innovation and financial inclusion. Despite this progress, local to global payment routes face challenges like high costs, fragmented networks, and a lack of global compliance. B2B payment systems have received different acceptance levels throughout the world. While some corridors are highly adopted, others are relatively low.

IT services and consulting firms, particularly in East Africa, lose business with global teams at various payment friction points like late settlements or failed callbacks. Even with payment aggregators, businesses witness cash flow problems that lead to significant customer service difficulties. However, you no longer require secondary options for global payments from and to Africa.

Together, let’s dive into how you can bridge the payment gap, enabling your local business to seamlessly expand into the global market.

The global-to-local B2B payment gap in East Africa

Despite the significant growth in financial inclusion, over 400 million adults in sub-Saharan Africa are still excluded from the formal economy and rely heavily on cash or informal providers. This gap creates unique challenges for East African IT teams looking to serve global clients or find vendors wanting to invest in the region.

Here are some of the common challenges with global-to-local routes in East Africa:

Payments often get stuck with the corresponding bank or wire transfer delays, leading to slow settlement into business accounts.

During online transactions, like e-commerce payments, the customer's account may be successfully debited. However, if the payment channel fails to reliably inform the service provider (the "callback"), the provider is left uncertain as to whether the payment was truly successful and therefore hesitant to deliver the service. This frequently causes major customer service issues.

In the world of payments, problems are a frequent occurrence, typically 5 to 10 out of every 1,000 transactions runs into an unprecedented issue. Businesses either struggle to efficiently manage exceptions like responding to queries, processing reversals, handling refunds, or lack a resolution.

Limitations with payment aggregators for East African businesses

While payment aggregators are commonly used by businesses for digital transactions in East Africa, including markets like Tanzania, this approach comes with its drawbacks. A significant issue is the prolonged duration for which aggregators hold payments. Poor customer service is a common challenge when managing inevitable exceptions such as slow response times, handling refunds, or payment reversals. This severely harms a business's reputation and contributes to customer churn for IT businesses.

Apart from the FX uncertainty, wire transfer delays and lack of trust in local rails, the webhooks (notifications of payment success) are unreliable across different providers. Businesses notice reconciliation breaking due to asynchronous settlement cycles. The main hurdle with the aggregators is that businesses can fail to employ a single API covering global and local payments together.

Let’s look at the most common scenarios where deals are lost:

Scenario A: payment friction

Digging into the details of the delayed payment, a regional tech startup in Nairobi had their payment to a remote software developer stuck. The developer's preferred mobile money system had a daily limit that was too low for the final invoice amount. The startup had to attempt the transfer over multiple days, causing a two-week delay in contract finalization and nearly derailing the project launch. The developer, frustrated by the lack of timely funds, almost pulled out of the deal entirely.

Scenario B: currency inflexibility

A Tanzanian IT consulting firm, fresh off a successful pitch to a major European NGO, lost the lucrative contract during the invoicing phase. The NGO required all invoices to be submitted in Euros (EUR) to simplify their cross-border budget tracking. The local firm's accounting system and bank could only process invoices in Kenyan Shillings (KES) or US Dollars (USD) without incurring significant, unmanageable compliance risk and hefty conversion fees. Unable to meet the EUR requirement efficiently, the NGO decided to award the contract to a competing South African firm that offered multi-currency invoicing as standard.

The current payment flow looks like:

Client → Gateway → Local Rail → Settlement

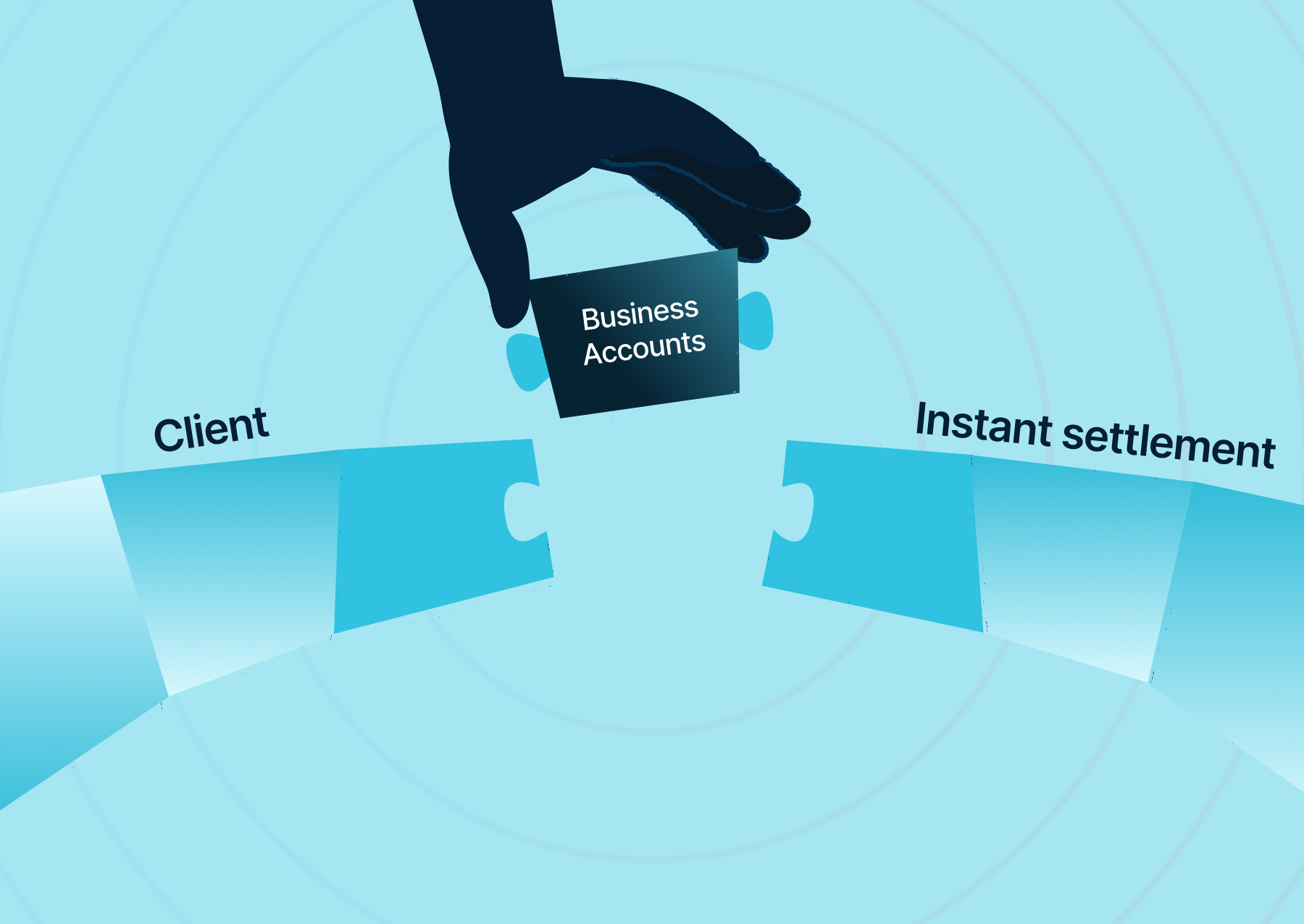

A modern Verto payment flow:

Client → Verto Business account → Instant settlement

The checklist for seamless payments

To successfully scale globally, East African businesses require a payment system built on four pillars: Capabilities to accept payments easily, Handle cross-border invoicing, Provide reliable settlement timelines, Compliant billing entities

When competing on the global stage, East African IT and consulting firms must move beyond fragmented local payment solutions and adopt a unified, reliable, and globally compliant payment infrastructure. Preparing for this transition requires a proactive assessment of the finance department's current capabilities, processes, and technological stack.

Evaluate your current payment landscape against these critical criteria:

Do you rely on a single, integrated payment platform for global or local operations, or do you manage a collection of disparate local bank accounts and providers?

Can your current system facilitate instant or near-instant payments between East African countries (e.g., Kenya, Tanzania, Uganda) and international partners (e.g., Europe, US) at the same time?

Is your payment infrastructure fully compliant with international anti-money laundering (AML), Know Your Customer (KYC) standards, and local tax regulations across all operating countries?

Is financial data automatically reconciled and standardized across all regional transactions, providing real-time visibility into cash flow and currency exposures?

Can your current payment infrastructure easily handle a 5x increase in transaction volume without requiring major re-engineering?

Are you able to benchmark transaction fees and foreign exchange (FX) rates competitively?

How Verto makes this happen

Global account

Verto's business accounts are designed for effortless international payments, allowing you to send and receive funds instantly in over 50 currencies. You can eliminate hidden exchange rates, administrative, and account fees. Our service supports sending and receiving money in 25 currencies, including local African currencies like NGN, KES, and ZAR, across 40+ countries. International money transfers are also supported via SWIFT.

Embed API-led infrastructure

Covering over 50 currencies, Verto offers confident market access and the necessary compliance structures for handling your transactions.

We provide an API-led embedded finance solution that serves as a comprehensive infrastructure for tackling complex payment issues. Trusted by platforms such as Triply, it ensures an ideal customer experience for their users.

Discover how Triply uses Verto Atlas

A world-class financial operation needs to be the engine, not the bottleneck, for global expansion. Is your finance team ready for the next phase of African development? Sign up with Verto today!

Share this article